Money vs. Wealth: Understanding the Critical Difference That Defines Financial Success in the U.S. Economy

WEALTH

1.1 What Is Money?

Money refers to the medium of exchange used to buy goods and services. In the United States, this usually means U.S. dollars whether in your checking account, savings account, or cash in hand. From a technical standpoint, money functions as a:

Medium of exchange: accepted for transactions

Unit of account: a standard measure of value

Store of value: retains value over time

These aspects make money immediately useful for daily life but it has limitations. Money in hand can be spent, saved, or invested, but by itself, it doesn’t automatically generate additional value.

1.2 What Is Wealth?

Wealth is a broader and more powerful concept. It refers to the total net worth of an individual, household, or nation. Net worth equals:

Assets (what you own) – Liabilities (what you owe) = Wealth (Net Worth)

Assets can include:

Real estate

Stocks, bonds, and investments

Retirement accounts

Business ownership

Intellectual property

Unlike simple money (cash or bank balances), wealth captures all things of economic value and the ability to generate future income or appreciation. Economists define wealth as “an abundance of valuable financial assets or physical possessions which can be converted into a form that can be used for transactions.”

2.Why Wealth Matters More Than Money

Money alone doesn’t guarantee long-term financial security. Wealth does.

2.1 Money Is Fluid; Wealth Endures

You can have money right now—but you can spend it, lose it, or see it eroded by inflation. Wealth, on the other hand, provides financial endurance.

Example:

Two individuals each receive $100,000.

Person A spends the money on a luxury vacation and lifestyle upgrades.

Person B invests in real estate and a diversified portfolio.

At the end of 10 years:

Person A may have little to show for that money.

Person B’s investments may have appreciated significantly, generating wealth that continues to compound.

This is the core difference: money can be transient, but wealth can be self-sustaining.

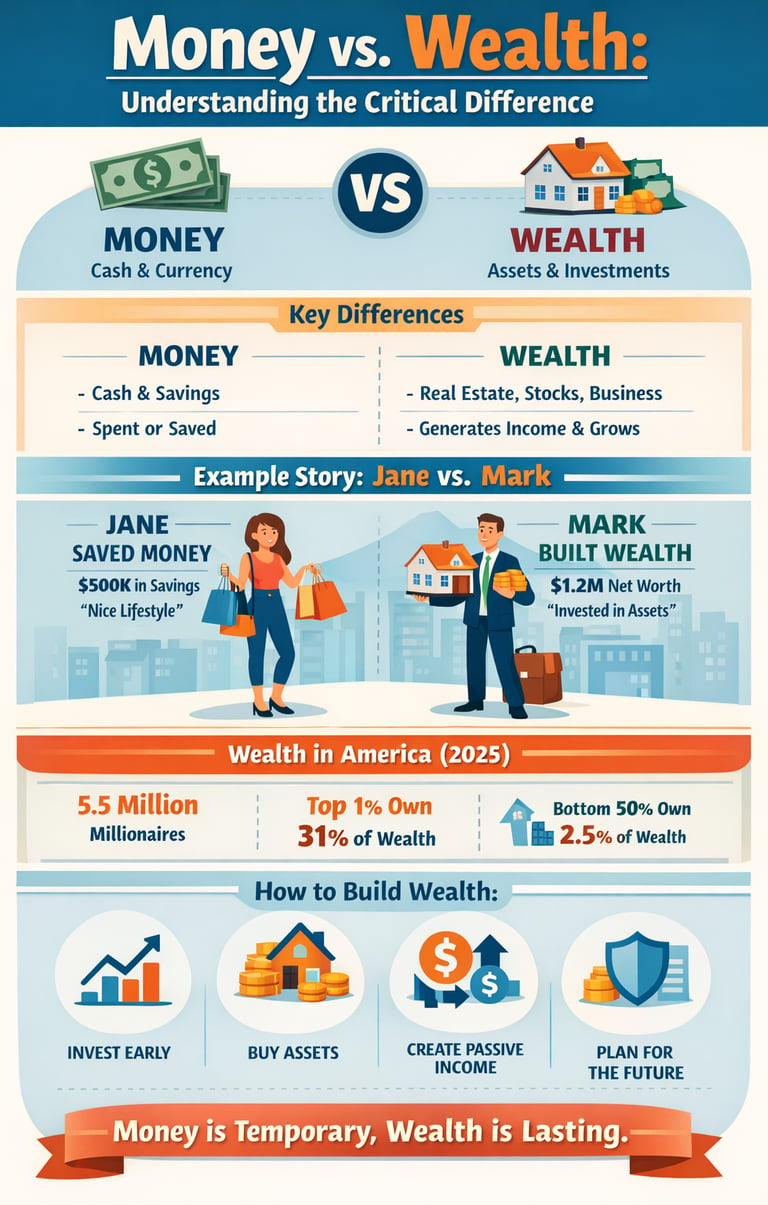

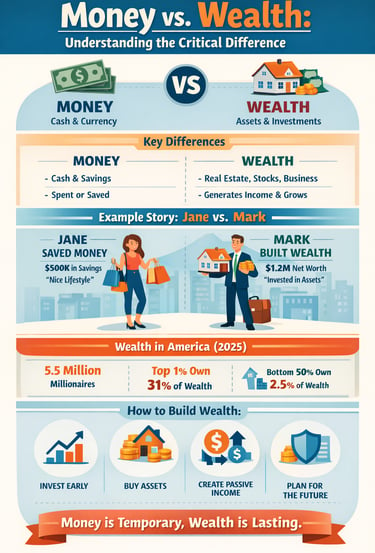

3.A Story That Makes It Real: Meet Jane and Mark

To illustrate this distinction, consider two fictional friends: Jane and Mark.

3.1 Jane’s Money-First Approach

Jane graduated college and immediately focused on earning money. She landed a solid job, saved every dollar she could, and enjoyed upgrading her lifestyle—nice dinners, new gadgets, and regular vacations.

By age 40:

Jane had $500,000 in money saved (in bank accounts and short-term investments).

But she had few assets that generated income.

She had no business, no rental properties, and little retirement planning.

If Jane were to retire early, she might find that her money doesn’t last as long as she hoped.

3.2 Mark’s Wealth-Building Strategy

Mark took a different route. He also earned a good income, but when he started his job he:

Bought a small rental property

Contributed regularly to retirement accounts

Invested in a low-cost index fund

Built a small online business that earned passive income

By age 40:

Mark’s net worth (wealth) was $1.2 million

His assets continued to generate income beyond his salary

Though Jane had high savings, Mark’s wealth provided both security and growth potential.

This story illustrates the real difference in strategy: money is earned, but wealth is built.

4. Wealth and Money in the United States: Current Data (2025)

Understanding how wealth is distributed gives context to the difference between money and wealth at a macro level.

4.1 Wealth in America Today

The United States holds over $67 trillion in liquid investable wealth more than any other country.

The U.S. is home to approximately 5.5 million millionaires (individuals with $1 million or more in investable assets).

Average wealth per person in the U.S. is about $565,000, but median wealth (which reduces outlier distortion) is about $112,000 showing a stark gap between average and typical household wealth.

This difference between average and median wealth underscores inequality: a relatively small number of very wealthy individuals pull the average upward, while most households have much less net worth.

4.2 Wealth Inequality in the U.S.

The top 1% of U.S. households hold nearly 31% of all wealth.

The bottom 50% of households hold only about 2.5% of total wealth.

Millionaire growth has been strong, with more than 1,000 new millionaires added every day in 2024 across the country.

These figures reflect how wealth concentration differs dramatically from simple money metrics like income or savings, and why understanding net worth wealth is so critical.

5. Why People Confuse Wealth and Money

There are several reasons the terms are conflated:

Language Simplicity: People use “money” to mean anything of value.

Short-Term Focus: Immediate cash balances are easier to observe than net worth.

Lack of Financial Education: Many consumers are taught to track spending and saving not asset building.

But one key financial truism remains: money buys things today; wealth buys freedom tomorrow.

6. How to Build Wealth, Not Just Money

Here are proven strategies to transition from earning money to building wealth:

6.1 Invest Early and Often

Compound growth rewards time in the market. Investing in retirement accounts or diversified funds increases net worth over time.

6.2 Acquire Income-Producing Assets

Assets like rental property, business ownership, dividends, and royalties can generate cash flow without active labor.

6.3 Protect Your Wealth

Insurance, estate planning, and tax-efficient strategies help preserve wealth over generations.

6.4 Think Long-Term

Wealth accumulation is a marathon, not a sprint. Smart financial planning emphasizes sustainability.

Conclusion: Money Is a Tool Wealth Is the Destination

Understanding the difference between money and wealth is not just semantic it changes how you make financial decisions. Money lets you live today; wealth assures your future. In the U.S., where wealth inequality is a defining economic feature, distinguishing these concepts can help individuals chart smarter financial journeys.

Start treating money as the fuel and wealth as the engine that drives long-term financial success.